NECA Alert: "One Big Beautiful Bill" Passes House

Early this morning, the House of Representatives passed H.R. 1, officially named the “One Big Beautiful Bill Act,” a sweeping tax reform package that extends and expands key provisions from the 2017 Tax Cuts and Jobs Act (TCJA) while introducing expanded tax breaks and other new measures. The bill now moves to the Senate for its consideration. As passed by the House, this legislation also addresses the State and Local Tax (SALT) deduction and modifies several energy-related tax credits from the Inflation Reduction Act (IRA). Below, we have outlined the changes to the SALT deduction, business tax provisions (Section 199A, Section 179, etc.), updates to specific energy tax credits, and the next steps for the bill.

Key Business Tax Changes

The bill delivers pro-growth tax policies to benefit NECA contractors:

- Section 199(a) –Qualified Business Income (QBI) Deduction for S-Corporations: Made permanent and increased from 20% to 23%, reducing the effective tax rate to 28.49% starting in 2026.

- Section 179(b) – Expensing Limits: Increased to $2.5 million (from $1.29 million), with a phase-out threshold of $4 million, both indexed for inflation starting after 2024.

- Bonus Depreciation (Section 168(k)): Restores 100% bonus depreciation for qualified property through 2029, reversing the current phase-down (40% in 2025).

- R&D Expensing (Section 174): Allows full 100% expensing of domestic R&D costs for 2026–2029, instead of five-year amortization.

- Business Interest Expense Deduction (Section 163(j)): Uses EBITDA instead of EBIT for calculating adjusted taxable income, increasing deductions for 2025–2029.

- Form 1099 Reporting Threshold: Raised from $600 to $2,000, indexed for inflation, starting in 2026, reducing administrative burdens.

- Other Provisions: Includes no tax on tips/overtime for incomes below ~$160,000 (expiring 2028) and a 25% interest exclusion for agricultural loans (enactment through 2028).

Estate and Gift Tax Changes

The estate and gift tax exemption is increased and permanently set at $15 million per person ($30 million for couples), indexed for inflation starting in 2026, supporting generational transfers of family-owned businesses.

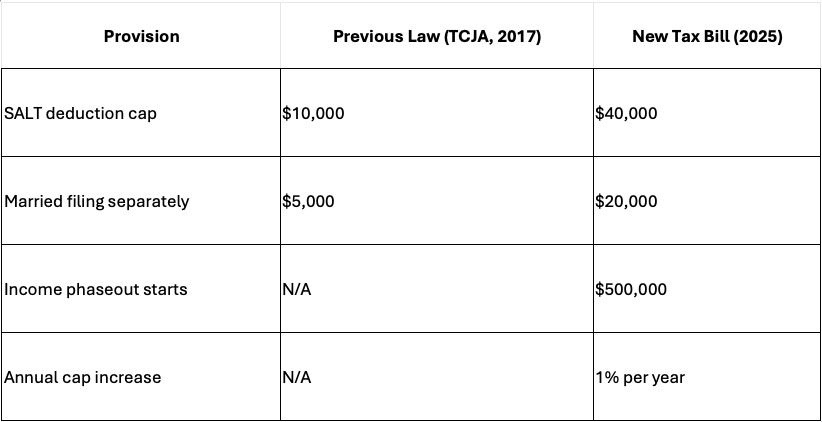

Overview of Changes to the SALT Deduction

The bill significantly reforms the State and Local Tax (SALT) deduction, which was previously capped at $10,000 ($5,000 for married individuals filing separately) under the TCJA through 2025.

Key changes include:

- Increased Cap: The SALT deduction cap is raised from $10,000 to $40,000 per household for tax years 2025 through 2029, indexed for inflation starting in 2026. For married taxpayers filing separately, the cap is set at $20,000

- Income Phase-Out: The increased deduction is subject to a phase-out for taxpayers with adjusted gross income (AGI) exceeding $500,000 ($250,000 for married individuals filing separately). The deduction reduces by $1 for every $2 of AGI above this threshold, effectively phasing out completely for higher earners.

- Impact for NECA Members: This change provides relief for contractors in high-tax states, allowing greater deductions for state and local income, property, and sales taxes, potentially freeing up capital for business investments. However, the phase-out may limit benefits for some high-income members.

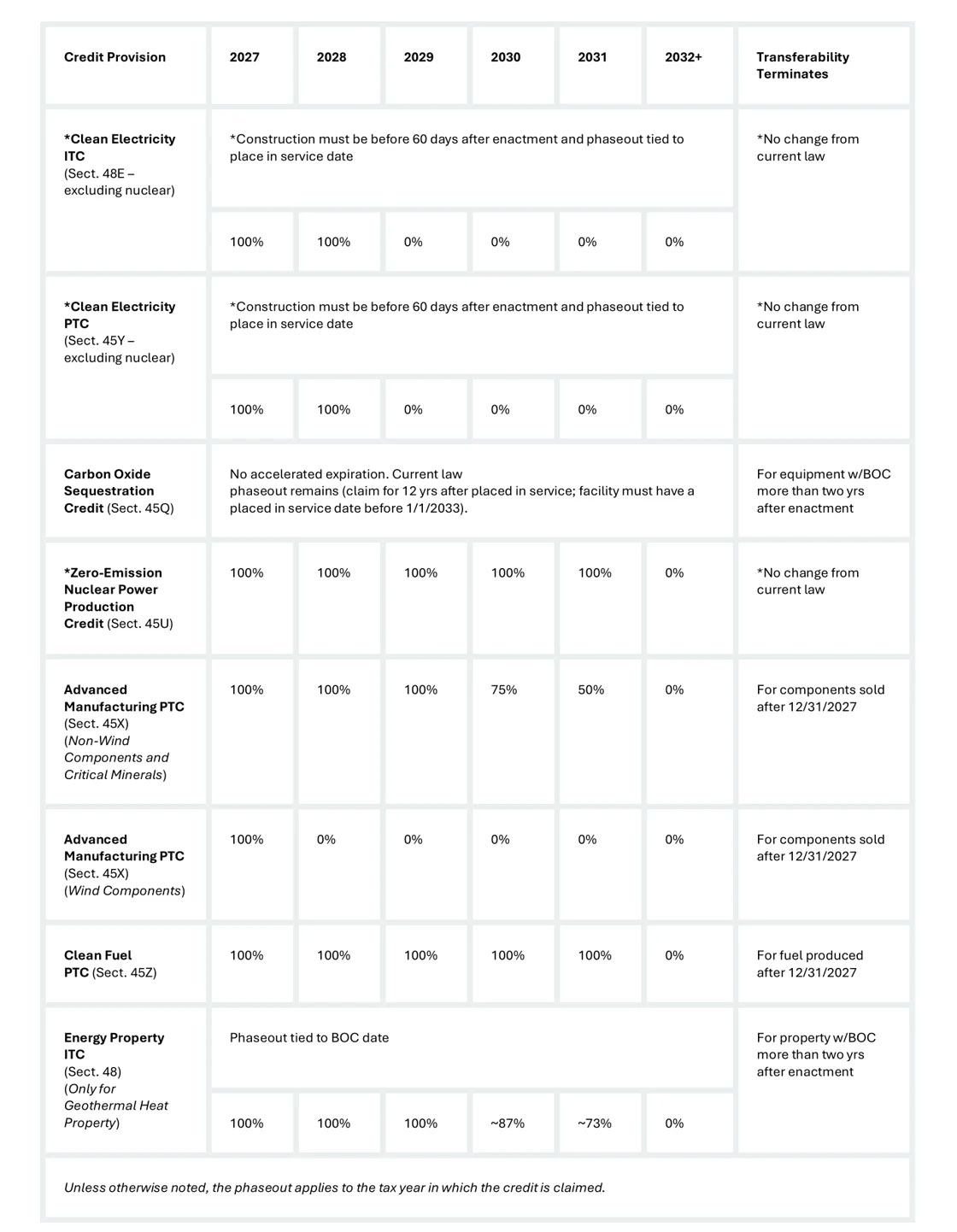

Inflation Reduction Act (IRA) Tax Credits

The legislation makes several modifications to the IRA energy tax credits, which could impact NECA members involved in clean energy projects. The bill in its current form would effectively repeal or sharply curtail most of the IRA’s clean energy tax credits, with many credits scheduled to end at the close of 2025. This would halt or reverse much of the clean energy investment and production boom triggered by the IRA since 2022. Below are details of some of the key provisions:

Tax Credits Modified and Preserved:

- Advanced Manufacturing Production Tax Credit (PTC) (Sect. 45X);

- Carbon Oxide Sequestration Credit (Sect. 45Q);

- Zero-Emission Nuclear Power Production Credit (Sect. 45U);

- Energy Property Investment Tax Credit (ITC) for Geothermal Heat Property (Sect. 48), and;

- Clean Fuel PTC (Sect. 45Z);

- NOTE: The Clean Fuel (PTC) ( 45Z) is the only surviving credit that would be extended (it was scheduled to terminate at the end of 2027 but would be extended an additional four years under the legislation.)

Tax Credits to be Eliminated:

- Clean Electricity PTC (Sect. 45Y) (safe harbor for projects with a construction start date before 60 days after enactment and have a placed in-service date before 2029); Clean Electricity ITC (Sect. 48E) (safe harbor for projects with a construction start date before 60 days after enactment and have a placed in-service date before 2029);

- Clean Hydrogen PTC (Sect. 45V) (safe harbor for projects with a construction start date before December 31, 2025);

- The following residential tax credits for energy efficiency and clean energy would generally expire at the end of 2025:

- Energy Efficient Home Improvement Credit (Sect. 25C)

- Residential Clean Energy Credit (Sect. 25D)

- New Energy Efficient Home Credit (Sect. 45L); and

- The following credits related to clean vehicles would generally expire at the end of 2025:

- Clean Vehicle Credit (Sect. 30D)

- Previously-Owned Clean Vehicles Credit (Sect. 25E)

- Alternative Fuel Vehicle Refueling Property Credit (Sect. 30C)

- Qualified Commercial Clean Vehicles Credit (Sect. 45W).

Next Steps for the Bill

The bill now heads to the Senate, where it faces scrutiny due to its $3.7–$3.8 trillion impact on federal borrowing. It is widely expected to go through several revisions, particularly to energy credit rollbacks and SALT provisions. NECA will be advocating for revisions to several of the IRA provisions. Once it passes the Senate, a conference committee will have to reconcile differences before a final vote later this summer.

NECA will advocate for contractor-friendly provisions, continue to keep you informed on new developments, and provide resources to navigate these changes.

Want to stay updated on Capitol Hill news and its impact on NECA Members? Subscribe to our Government Affairs newsletter below.